Ultimate Guide to Lease Accounting For New Controllers

Last Updated on June 6, 2024 by Morgan Beard

As a new controller, understanding lease accounting is pivotal to your role, especially with the intricacies introduced by ASC 842. This guide will walk you through the key steps and considerations for lease accounting for new controllers, ensuring compliance and accuracy in financial reporting.

Introduction to ASC 842

ASC 842, implemented by the Financial Accounting Standards Board (FASB), mandates that lessees recognize most leases on the balance sheet as a right-of-use (ROU) asset and a lease liability. The classification of leases as either finance or operating impacts the pattern of expense recognition. ASC 842 aims to enhance transparency and comparability in a company’s performance, providing users of financial statements with a clearer understanding of leasing activities and their financial impact.

Step-by-Step Guide to Lease Accounting under ASC 842

Step 1: Identifying a Lease

The first step is to determine if an arrangement contains a lease. This involves evaluating contracts to see if they convey the right to control the use of an identified asset for a period of time in exchange for consideration. Pay special attention to embedded leases, where the right to use an asset is part of a larger arrangement, such as a service contract.

Step 2: Identifying the Lease Term

The lease term includes the non-cancelable period and any additional periods covered by options to extend or terminate the lease if they are reasonably certain to be exercised. Consider all relevant factors and contractual terms to ensure the lease term reflects the economic reality of the arrangement. Something being reasonably certain is a higher threshold than something being probable so make sure you can support your decision when it comes to audit season.

Step 3: Determining the Lease Payments

Lease payments include fixed payments throughout the expected lease term, options to purchase the underlying asset, and most other types of fixed costs except taxes. Lessees should measure these payments at their present value using the rate implicit in the lease or, if that rate cannot be determined, the lessee’s incremental borrowing rate.

Step 4: Initial Recognition and Measurement

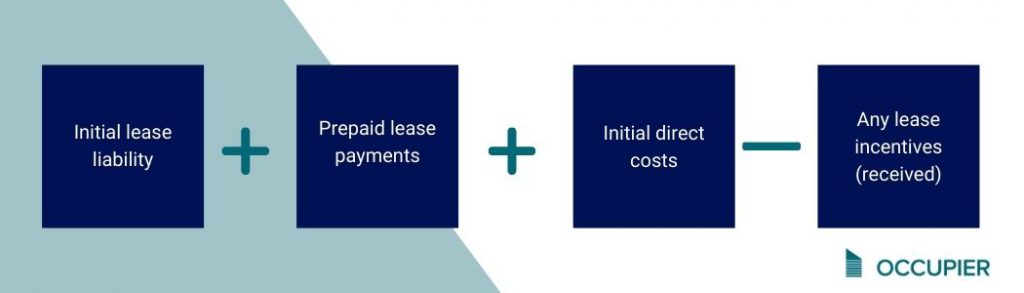

Recognize the lease liability and ROU asset on the balance sheet at the date you gain possession of the underlying asset. The lease liability is the present value of future lease payments leveraging your incremental borrowing rate. The ROU asset also considers prepaid rent, initial direct costs (like broker commissions), and any incentives (like tenant improvement allowance) paid before the commencement date.

On the possession date, you will also need to determine the lease classification: operating or finance. While this does not change the journal entries on the possession date, the lease classification dictates the subsequent expense recognition of the lease.

Right of Use Asset Calculation

Step 5: Subsequent Measurement and Expense Recognition

Monthly journal entries should adjust the lease liability for lease payments made. In addition, for finance leases, monthly journal entries should also recognize interest expense on the lease liability and amortize the ROU asset. For operating leases, recognize a straight-line lease expense over the lease term. If you perform monthly regulatory reporting, you will also want to perform a reclass entry between the current portion of the lease liability and long term to ensure the balance sheet classification is correct.

It is common for leases to be amended throughout the lease term. Whenever this happens, you will need to determine if the amendment should be treated as a separate lease or as a modification to the original lease. If the amendment provides the lessee with an additional ROU asset and the value of the contracts increases based on the value of that additional ROU asset, the lease will be treated as a separate lease. If a lease modification creates a separate lease, the lessee makes no adjustments to the original lease and accounts for the separate lease the same as any new lease.

Moreover, your company should be assessing for impairment in the ROU assets at least annually. Just like any other long lived asset, ROU Assets can be impaired due to a multitude of factors.

Step 6: Disclosures

ASC 842 expands disclosure requirements to enhance transparency. Disclosures include qualitative and quantitative information about leases, significant judgments and assumptions made, and additional narrative explanations to provide context. This helps users understand the nature, timing, and uncertainty of cash flows arising from leases.

Preparing for Your First Audit Under ASC 842

Transitioning to ASC 842 means significant changes in how leases are accounted for, which also impacts how audits are conducted. Auditors will focus on lease identification and modifications, ensuring that all leases are correctly identified and accounted for under the new standard. Maintain open communication with your auditors throughout the year. Promptly respond to audit requests and involve external service providers as needed. Lease accounting for new controllers often starts with an impending audit under ASC 842, so this is a great time to evaluate your organizations processes.

Lease Identification Issues

Auditors will verify that all leases have been identified that meet the ASC 842 definition. This includes identifying embedded leases within broader contracts. Ensure that all contracts are available for review, paying particular attention to high-value assets like production equipment and IT infrastructure. To reduce the lease identification risk, follow these tips:

- Gather all relevant contracts for auditors.

- Identify departments and personnel who can enter into lease-style contracts.

- Review general ledger accounts for standard payments.

- Determine lease and non-lease components within contracts.

Policies and Internal Controls

Auditors will assess your policies and internal controls related to ASC 842. Be prepared to demonstrate how you have implemented and maintained changes, and provide detailed documentation, including a Lease Accounting memo.

When documenting internal controls, identify lease accounting personnel, and provide a breakdown of duties. Common controls to have for your lease accounting process include:

- Reviewing all contracts entered into or modified to determine if a lease exists, as necessary

- Review the incremental borrowing rate utilized for all new and modified leases, as necessary

- Review the lease classification calculations to validate the lease classification, as necessary

- At least annually, assess for impairment of ROU assets

- Review change log history of lease accounting software monthly to ensure only expected changes were made by the appropriate personnel. Investigate any unexpected changes

- Review access to lease accounting software quarterly to determine if the appropriate personnel have access to the software. Remove or add members as necessary.

Streamlining the Process with Lease Accounting Software

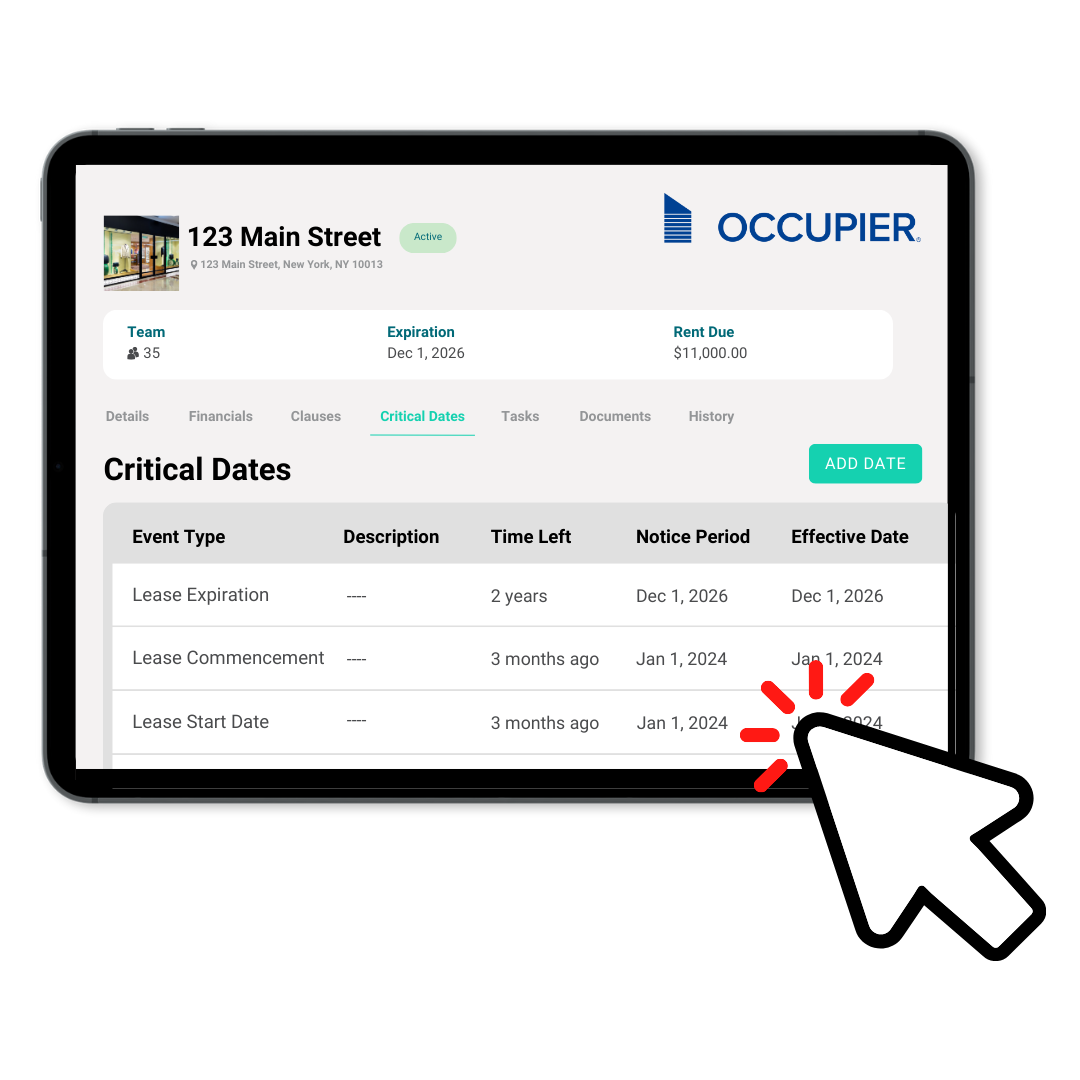

Manual processes and spreadsheets can be insufficient for handling the volume of lease data and ensuring compliance with ASC 842. Lease management software solutions, such as Occupier, offer centralized lease data storage, automated calculations, lease payment tracking, and comprehensive reporting capabilities. These solutions enhance efficiency, strengthen internal controls, and improve data accuracy.

Occupier provides a full-featured lease accounting system to ensure data quality and compliance with ASC 842. Occupier simplifies lease management, helping you stay prepared for audits year-round.

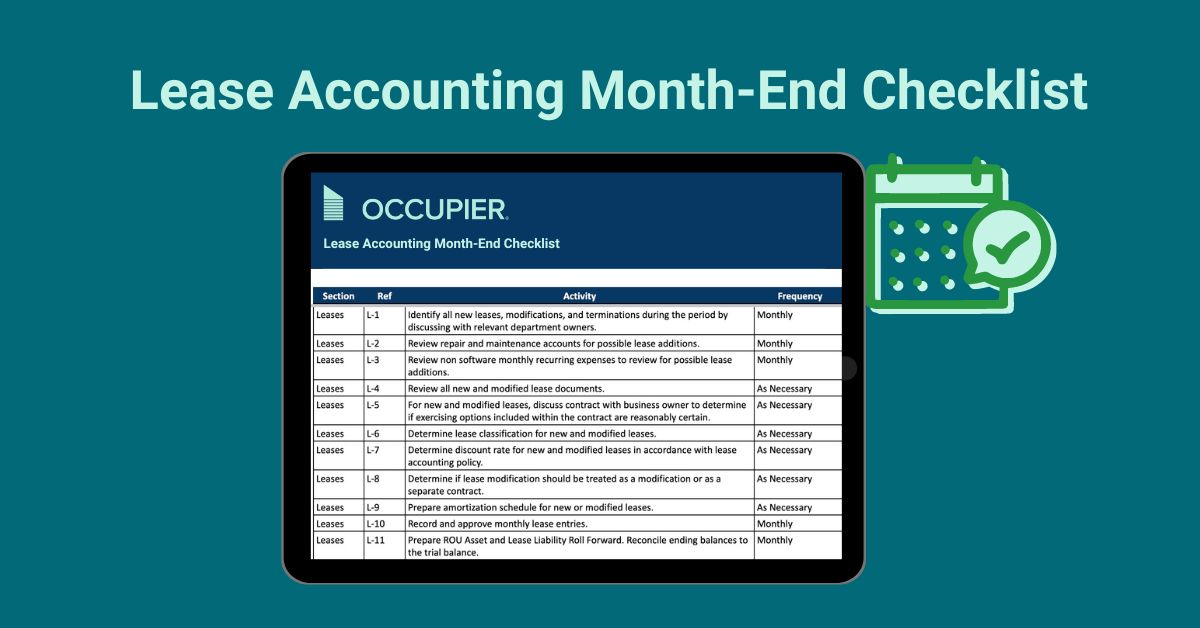

Month-End Checklist for Lease Accounting

To ensure accuracy and completeness in your month-end close, leverage a detailed lease accounting month-end checklist. This checklist should cover all areas of the financial statements but can be tailored for leases. Using this checklist ensures that all necessary activities are completed on time, maintaining the accuracy and reliability of your financial statements.

Looking for an easier way to navigate your month-end close process, check out Numeric.io, the AI powered close automation software, that streamlines reconciliations, and puts your monthly close on auto-pilot.

Lease Accounting For New Controllers

Navigating lease accounting under ASC 842 can be complex, but with the right tools and knowledge, it becomes manageable. Stay informed about the latest developments in lease accounting and consider utilizing lease management software solutions to simplify your processes. Lease accounting for new controllers can be eased by following the steps outlined in this guide to ensure compliance and accuracy in lease accounting, contributing to the overall financial health and transparency of their organizations.

Product Tour

Take a self-guided tour and see how the fastest-growing commercial tenants leverage Occupier for lease management & lease accounting.